Buying a new smartphone has become a necessity rather than a luxury. From premium iPhones and Samsung flagships to mid-range Vivo, Realme, and Redmi phones—EMI options make high-priced devices affordable for everyone. But when it comes to choosing the right EMI plan, buyers often face two popular options:

- No Cost EMI

- Standard EMI

Both allow you to pay monthly installments instead of paying the entire price upfront, but the total cost, monthly EMI amount, interest charged, and hidden fees can be drastically different.

Choosing the wrong plan can make your smartphone significantly more expensive over time.

Choosing the right one can help you save thousands.

In this detailed guide, we will break down everything you need to know about No Cost EMI vs Standard EMI, including formulas, examples, hidden charges, interest impact, lender comparison, and expert suggestions.

This is the most complete, beginner-friendly, long-form guide you will find—fully optimized for SEO and perfect for your blog.

What Is EMI & Why Does It Matter for Mobile Buyers?

EMI (Equated Monthly Installment) is a repayment method that allows you to buy a product by paying smaller fixed amounts every month.

Instead of paying ₹30,000–₹1,00,000 at once, EMI lets you break this into affordable monthly payments.

For mobile buyers, EMI is important because:

✔ It reduces upfront financial burden

✔ Makes premium smartphones more accessible

✔ Helps buyers manage monthly income better

✔ Offers multiple repayment options

✔ Allows students and low-income buyers to purchase phones

However, all EMI plans are not the same.

The type of EMI you choose decides the final price you pay.

Understanding No Cost EMI – What It Really Means

No Cost EMI means that the lender does not charge any interest on the loan.

Your EMI amount equals the phone’s price divided by the number of months.

✔ Simple No Cost EMI Example

Phone Price: ₹24,000

Tenure: 12 months

EMI = ₹24,000 ÷ 12 = ₹2,000 per month

You do not pay ₹1 extra.

This sounds magical—and for the buyer, it truly is.

But how do banks offer free EMI?

Why would they waive interest?

Let’s decode it.

How No Cost EMI Actually Works (Behind the Scenes)

There is a common misconception that the bank gives free loans.

That’s not true.

Here’s how No Cost EMI becomes possible:

✔ 1. The seller pays the interest

Brands like Samsung, Apple, Realme, or retailers like Amazon and Flipkart pay the bank the interest.

✔ 2. Discounts are adjusted

If a phone has a ₹2,000 discount, the seller may remove it to offer No Cost EMI.

✔ 3. Processing fees may apply

A small fee may be charged (but not always).

✔ 4. Credit card EMI partnerships

Banks offer special offers only for select cards.

In most genuine No Cost EMI plans, you truly pay zero interest—but you must check for hidden charges.

Standard EMI – The Traditional EMI Method Explained

Standard EMI is the typical EMI option provided by banks or finance companies.

In Standard EMI:

- Interest is charged

- Monthly EMI includes principal + interest

- Total payable amount increases

- Tenure flexibility is higher

Interest rates vary between 10% and 24%, depending on:

- Lender

- CIBIL score

- Tenure

- Phone model

- Credit card type

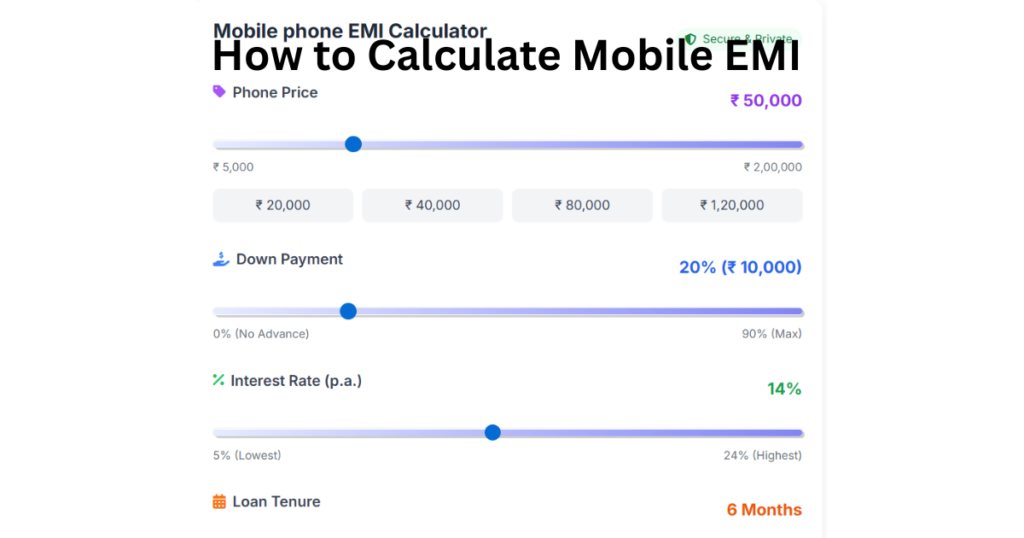

Standard EMI Example (With Real Numbers)

Phone Price: ₹50,000

Down Payment: ₹10,000

Loan Amount: ₹40,000

Interest Rate: 14%

Tenure: 12 months

Using the EMI formula:

Monthly EMI ≈ ₹3,575

Total Payment ≈ ₹42,900

Interest Paid = ₹2,900 extra

Final mobile cost = ₹52,900 instead of ₹50,000.

This is why understanding EMI differences is essential.

No Cost EMI vs Standard EMI – Side-by-Side Comparison

| Feature | No Cost EMI | Standard EMI |

|---|---|---|

| Interest Rate | 0% | 12%–24% |

| Monthly EMI | Lower | Higher |

| Total Cost | Same as product price | Higher than product price |

| Best For | Budget buyers | Buyers wanting longer tenure |

| Hidden Charges | Possible | Interest + fees |

| Tenure Options | Usually 3–12 months | 3–24 months |

| Eligibility | Selected buyers | Almost everyone |

| Payment Mode | Credit/debit/BNPL | Mostly credit card |

Is No Cost EMI Truly Free? (Hidden Truth Explained Clearly)

The term “No Cost EMI” sounds perfect, but there are some important things to check:

✔ Processing Fee

Some banks charge 1–3% processing fee even on No Cost EMI.

✔ GST on Charges

GST applies to processing and convenience fees.

✔ Discount Removal

Sellers may remove instant discounts when you choose No Cost EMI.

✔ Higher MRP

Some stores artificially increase the phone price to adjust interest costs.

✔ Only for select cards

Not all users qualify.

Conclusion: No Cost EMI is “free” only when there are NO processing fees + NO removed discounts + NO price adjustment.

Real-Life Example: No Cost EMI vs Standard EMI (Price Comparison)

Let’s evaluate both EMI types using an example.

⭐ Phone Price: ₹20,000

Scenario A: No Cost EMI (10 Months)

- Interest = 0%

- Processing = ₹0

- EMI = ₹20,000 ÷ 10 = ₹2,000

- Total cost = ₹20,000

Scenario B: Standard EMI (10 Months @ 14%)

Loan Amount = ₹20,000

Monthly EMI ≈ ₹2,310

Total Paid ≈ ₹23,100

Interest Paid = ₹3,100

✔ Savings with No Cost EMI = ₹3,100

No Cost EMI clearly wins.

When You Should Choose No Cost EMI

No Cost EMI is the best choice when:

✔ You want maximum savings

✔ EMI doesn’t change the total price

✔ You prefer short or medium tenure

✔ You are buying during Amazon/Flipkart sale

✔ You have a compatible card/BNPL option

✔ You have a tight budget

Perfect for:

- Students

- Young buyers

- Salary earners

- Budget-conscious users

When You Should Choose Standard EMI

Standard EMI is suitable when:

✔ No Cost EMI is not available

✔ You want longer tenure (15–24 months)

✔ You don’t want high monthly EMI

✔ You don’t have required credit card for No Cost EMI

✔ You are buying expensive flagship phones

This is ideal for:

- Buyers of premium iPhones

- Buyers who can’t pay much monthly

- Users who want greater flexibility

Top Lenders Offering No Cost & Standard EMI

Here are the best EMI providers:

No Cost EMI Providers

Bajaj Finserv EMI Card

HDFC Bank Credit/Debit Card EMI

ICICI Bank No Cost EMI

Amazon Pay Later

Flipkart Pay Later

ZestMoney

Home Credit

Standard EMI Providers

SBI Card EMI

SBI Card EMI

Kotak EMI

Axis Bank EMI

ICICI Bank EMI

HDFC EMI

NBFC mobile loans

Hidden Charges to Check Before Choosing EMI

Always review these factors:

✔ Interest rate

10–24% depending on lender.

✔ Processing fee

0–3% of loan amount.

✔ Down payment

Some plans require 10–40%.

✔ Foreclosure charges

Early closure may cost extra.

✔ GST

Charged on processing fees.

✔ Late payment penalty

Can exceed 30–40% annually.

Impact of EMI Tenure on Total Cost

Tenure significantly affects EMI:

✔ Short Tenure (3–6 months)

- Higher EMI

- Lowest interest

- Best financial decision

✔ Medium Tenure (9–12 months)

- Balanced EMI

- Moderate interest

- Most popular option

✔ Long Tenure (18–24 months)

- Lowest EMI

- Highest interest

- Good for premium phones

No Cost EMI vs Standard EMI – Which Saves More Money?

Winner: No Cost EMI (0% Interest)

You save the maximum because you pay only the phone’s original price.

Runner-up: Standard EMI (Interest Added)

Useful only when:

- Tenure needs to be long

- No Cost EMI unavailable

- You prefer smaller monthly payments

If saving money is your priority:

✔ Always choose No Cost EMI

If monthly EMI limitation is your priority:

✔ Choose Standard EMI with longer tenure

How to Check EMI Before Buying a Phone (Smart Buyer Method)

Before selecting any EMI:

- Open a Mobile EMI Calculator Online

- Enter phone price

- Add down payment

- Choose interest rate

- Select different tenures

- Compare EMI & total cost

- Check hidden fees

- Choose the best plan

This ensures transparency and avoids financial shocks.

Frequently Asked Questions (FAQ)

Q1. Which EMI is better for mobile buyers?

No Cost EMI is always better financially, if no hidden fees are present.

Q2. Is Standard EMI bad?

Not bad—just more expensive because of interest.

Q3. Can I take EMI without a credit card?

Yes. Bajaj, ZestMoney, Home Credit, Amazon Pay Later, Flipkart Pay Later—all allow it.

Q4. Does EMI affect credit score?

Regular EMI payments improve your credit score.

Q5. Does No Cost EMI really save money?

Absolutely. As long as no processing fee is charged.

Final Verdict – Which EMI Should You Choose?

Here is the final, clear answer:

⭐ Choose No Cost EMI if:

✔ You want maximum savings

✔ You have the eligible card/BNPL option

✔ Tenure of 3–12 months is comfortable

⭐ Choose Standard EMI if:

✔ You need longer tenure (18–24 months)

✔ No Cost EMI is unavailable

✔ You want smaller monthly EMI

Before finalizing your purchase, always use a mobile EMI calculator to compare interest, EMI, and total cost for different lenders.

This simple step can save you thousands of rupees—and help you choose the most budget-friendly EMI option for your smartphone.