Buying a new mobile phone on EMI has become extremely common in India and around the world. Whether it’s a flagship iPhone, a Samsung Galaxy, a Vivo camera phone, or a budget-friendly Realme device, EMI makes expensive phones more affordable by converting the price into easy monthly installments.

However, many buyers do not understand how to calculate mobile EMI , what factors affect EMI, and how banks or finance companies determine interest. This lack of clarity leads to confusion, especially when comparing different EMI options such as No Cost EMI, Standard EMI, Debit Card EMI, Credit Card EMI, and BNPL (Buy Now Pay Later) EMI programs.

This guide explains step-by-step how to calculate mobile EMI, both manually and using an online EMI calculator. By the end of this article, you will clearly understand EMI calculations, interest components, tenure selection, and how to choose the best plan before buying a mobile phone.

⭐ What Is Mobile EMI and How Does It Work?

Mobile EMI (Equated Monthly Installment) is a financing method that allows you to purchase a mobile phone by paying monthly installments instead of paying the entire amount upfront.

The EMI remains constant each month and includes:

- Principal amount (loan amount)

- Interest amount

- Any additional charges (if applicable)

Meaning of EMI (Equated Monthly Installment)

EMI is the fixed amount you pay every month toward your loan. It includes both repayment of the principal amount and the interest cost.

Example:

If you buy a phone worth ₹40,000 on EMI for 12 months, you will pay a fixed amount every month until the full amount (principal + interest) is paid off.

Components Included in EMI Calculation

To calculate EMI, lenders consider:

✔ Loan Amount

This is the amount financed after deducting the down payment.

✔ Interest Rate

Banks and NBFCs charge annual interest (e.g., 12%, 14%, 18%).

✔ Tenure (Months)

The duration (3, 6, 9, 12, 18, 24 months) over which EMI is paid.

✔ Processing Fees (Optional)

Some lenders charge 1–3% of the loan amount.

Why EMI Calculation Is Important Before Buying a Mobile

Most buyers make the mistake of accepting EMI plans without checking:

- Total interest paid

- Total cost of the phone

- Difference between EMI options

- Impact of tenure change

A mobile EMI calculator helps you avoid unnecessary interest and choose the right EMI plan tailored to your budget.

⭐ Formula Used to Calculate Mobile EMI

Banks and finance companies use a standard mathematical formula to calculate EMI.

EMI = [P × R × (1 + R) ^ N] / [(1 + R) ^ N – 1]

Where:

- P = Principal loan amount

- R = Monthly interest rate (Annual Rate / 12 / 100)

- N = Tenure in months

Example:

Annual interest = 12% → Monthly interest = 1% or 0.01

What Each Component Means (P, R, N)

✔ P (Principal):

Loan amount = Phone price – Down payment

✔ R (Rate):

Interest rate divided by 12 months

✔ N (Tenure):

Number of monthly installments

Why Manual EMI Calculation Is Hard

The EMI formula uses exponents and complex interest calculations.

Doing it manually is time-consuming and error-prone.

That’s why Mobile EMI Calculators Online are the easiest way to calculate EMI instantly.

⭐ How to Calculate Mobile EMI Manually (Step-by-Step)

Even though online calculators make it easy, understanding the manual method helps you make smarter financial decisions.

Let’s break this down in simple steps. how to calculate mobile emi.

Step 1 – Find the Loan Amount

Loan Amount = Phone Price – Down Payment

Example:

Phone Price = ₹50,000

Down Payment = ₹10,000

Loan Amount = ₹40,000

Step 2 – Convert Annual Interest to Monthly Interest

If the lender charges 12% annually:

Monthly interest = (12/12)/100 = 1% or 0.01

If interest is 14% annually:

Monthly interest = (14/12)/100 = 1.166% or 0.01166

Step 3 – Apply the EMI Formula

Insert P, R, and N into the formula.

Example:

P = ₹40,000

R = 0.01166 (for 14%)

N = 6 months

Use the EMI formula to calculate monthly EMI.

Step 4 – Calculate Total Interest & Total Cost

Total EMI paid = EMI × N

Total interest = Total EMI – Loan Amount

Total cost = Loan Amount + Total Interest + Down Payment

Example Manual EMI Calculation (With Real Values)

Loan Amount: ₹40,000

Interest Rate: 14%

Tenure: 6 Months

Monthly EMI (approx.) = ₹6,942

Total Interest = ₹1,649

Total Cost = ₹51,649

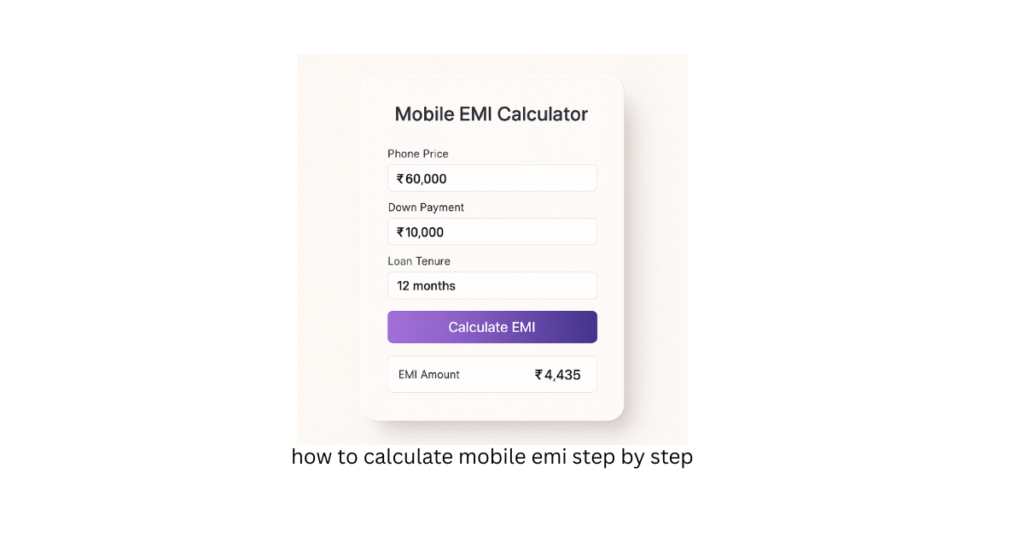

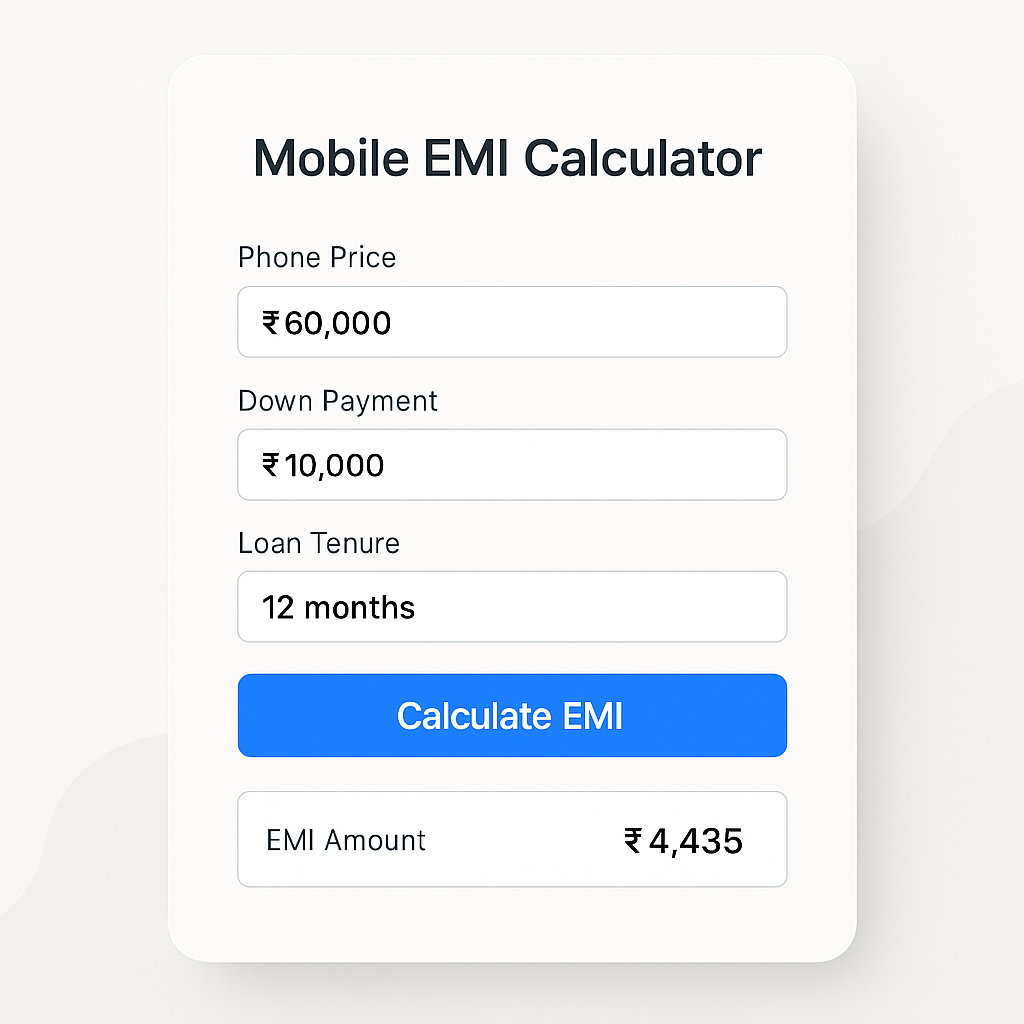

⭐ How to Calculate Mobile EMI Using an Online EMI Calculator

Calculating EMI manually is complicated.

A Mobile EMI Calculator Online gives results instantly and accurately.

Here’s how to use it:

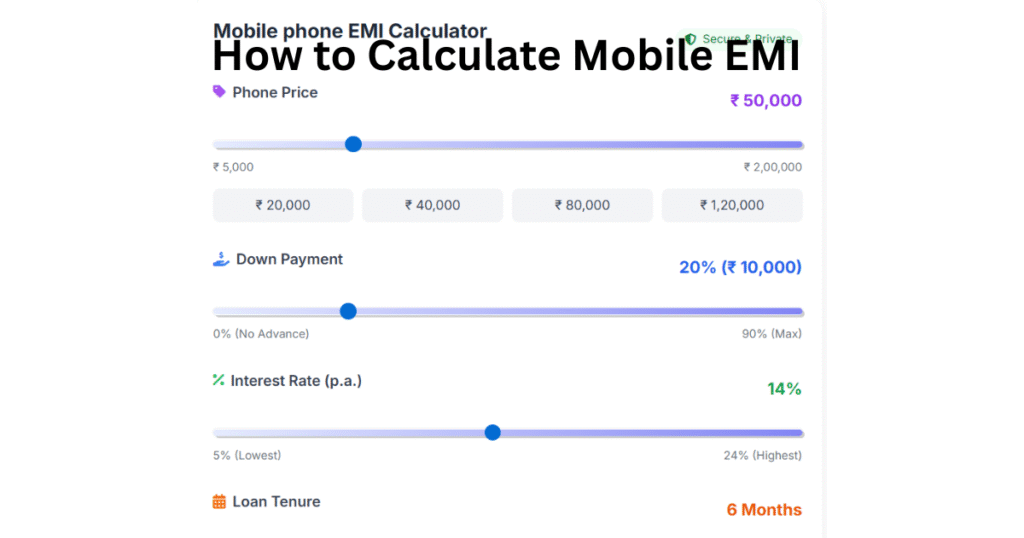

Step 1 – Enter the Mobile Price

Use the slider or input box.

Example: ₹50,000

Step 2 – Enter Down Payment

Sliders allow quick adjustments.

Example: 20% = ₹10,000

Step 3 – Select Loan Tenure

Choose from:

- 3 months

- 6 months

- 12 months

- 18 months

- 24 months

In the sample UI, 6 months is selected.

Step 4 – Enter Interest Rate

Banks/NBFCs typically charge 10%–24%.

Your example: 14%

Step 5 – Click “Calculate EMI”

The calculator shows:

✔ EMI

✔ Total cost

✔ Total interest

✔ Loan amount

✔ EMI schedule

Benefits of Using an Online EMI Calculator

✔ Instant results

✔ Accurate calculations

✔ Shows total interest

✔ Compares EMI for different tenures

✔ Provides amortization schedule

✔ Helps avoid hidden charges

✔ Saves time

This is the fastest and most reliable method for EMI comparison.

⭐ Mobile EMI Example Calculations for Different Tenures

Let’s take a phone with:

- Price: ₹50,000

- Down Payment: ₹10,000

- Loan: ₹40,000

- Interest: 14%

Here’s how EMI differs with tenure:

| Tenure | Monthly EMI | Total Interest | Total Cost |

|---|---|---|---|

| 3 Months | High EMI | Low interest | Lower cost |

| 6 Months | ₹6,942 | ₹1,649 | ₹51,649 |

| 12 Months | Lower EMI | Higher interest | Higher cost |

| 24 Months | Lowest EMI | Highest interest | Maximum cost |

⭐ Factors That Affect Your Mobile EMI

Your EMI can vary based on:

✔ Phone Price

Higher the price → higher the EMI.

✔ Down Payment

More down payment → less loan → lower EMI.

✔ Interest Rate

Higher interest → more cost.

✔ Tenure

Longer tenure → lower EMI but more interest.

✔ Processing Fees

Some lenders charge up to 3% processing fee.

⭐ How EMI Changes Based on Tenure

✔ Short Tenure = High EMI, Low Total Interest

Best for people who want to save money.

✔ Long Tenure = Low EMI, High Total Interest

Best for those with tight monthly budgets.

✔ Ideal Tenure

For most users: 6–12 months

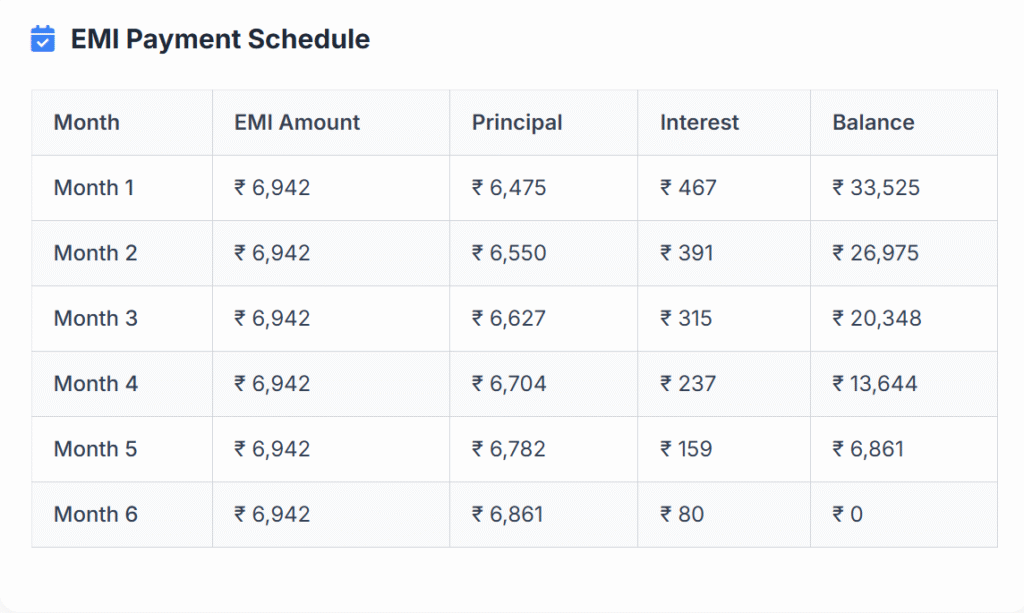

⭐ Understanding the EMI Payment Schedule

The EMI calculator generates an amortization schedule showing:

- EMI

- Principal paid

- Interest paid

- Balance remaining

This breakdown reveals how your loan decreases monthly.

Month-by-Month EMI Example

| Month | EMI | Principal | Interest | Balance |

|---|---|---|---|---|

| 1 | ₹6,942 | ₹6,451 | ₹491 | ₹33,549 |

| 2 | ₹6,942 | ₹6,492 | ₹450 | ₹27,057 |

| 3 | ₹6,942 | ₹6,533 | ₹409 | ₹20,524 |

| 4 | ₹6,942 | ₹6,575 | ₹367 | ₹13,949 |

| 5 | ₹6,942 | ₹6,617 | ₹325 | ₹7,332 |

| 6 | ₹6,942 | ₹6,669 | ₹273 | ₹663 |

⭐ No Cost EMI vs Standard EMI – Detailed Comparison

What Is No Cost EMI?

A financing option where interest is zero.

✔ Pros:

- No interest

- EMI = actual phone price ÷ tenure

- Best during online sales

✔ Cons:

- GST may apply on processing fee

- Not available for all phones

What Is Standard EMI?

Regular EMI includes interest based on bank rates.

✔ Pros:

- Available everywhere

- Flexible tenure options

✔ Cons:

- Higher total cost

- Interest + processing fees

Which EMI Type Saves More Money?

No Cost EMI always saves more because there is no interest.

If No Cost EMI is unavailable, choose:

- Higher down payment

- Shorter tenure

- Lower interest lender

⭐ Tips to Reduce EMI While Buying a Mobile

✔ Increase down payment

✔ Choose shorter tenure

✔ Compare interest rates

✔ Check for No Cost EMI offers

✔ Avoid unnecessary add-ons

✔ Buy during festival sales

✔ Use Debit Card EMI or BNPL if cheaper

⭐ Frequently Asked Questions (FAQ)

Q1. Can I calculate EMI without a calculator?

Yes, but it is complex. Using an online EMI calculator is easier.

Q2. How accurate is the EMI calculator?

It uses the same formula banks follow—100% accurate.

Q3. Does EMI increase the mobile’s price?

Standard EMI increases total cost due to interest.

No Cost EMI does not.

Q4. What is the minimum CIBIL score required?

Generally 650+, but BNPL apps approve even lower scores.

Q5. Can students buy mobiles on EMI?

Yes, using ZestMoney, Home Credit, Amazon Pay Later, Flipkart Pay Later.

⭐ Final Thoughts – Why You Should Always Calculate EMI Before Buying a Phone

Calculating EMI before buying a smartphone is essential for making a smart financial decision. It ensures:

- No surprises in monthly payments

- Clear understanding of interest

- Proper budget planning

- Transparent loan breakdown

- Better comparison between EMI providers

A Mobile EMI Calculator Online makes this process effortless, helping you find the most affordable and stress-free EMI plan.

Use the calculator before every mobile purchase to save money, avoid hidden charges, and choose the perfect EMI option for your budget.